9. Some Probability Distributions#

This lecture is a supplement to this lecture on statistics with matrices.

It describes some popular distributions and uses Python to sample from them.

It also describes a way to sample from an arbitrary probability distribution that you make up by transforming a sample from a uniform probability distribution.

In addition to what’s in Anaconda, this lecture will need the following libraries:

!pip install prettytable

As usual, we’ll start with some imports

import numpy as np

import matplotlib.pyplot as plt

import prettytable as pt

from mpl_toolkits.mplot3d import Axes3D

from matplotlib_inline.backend_inline import set_matplotlib_formats

set_matplotlib_formats('retina')

9.1. Some Discrete Probability Distributions#

Let’s write some Python code to compute means and variances of some univariate random variables.

We’ll use our code to

compute population means and variances from the probability distribution

generate a sample of

compare population and sample means and variances

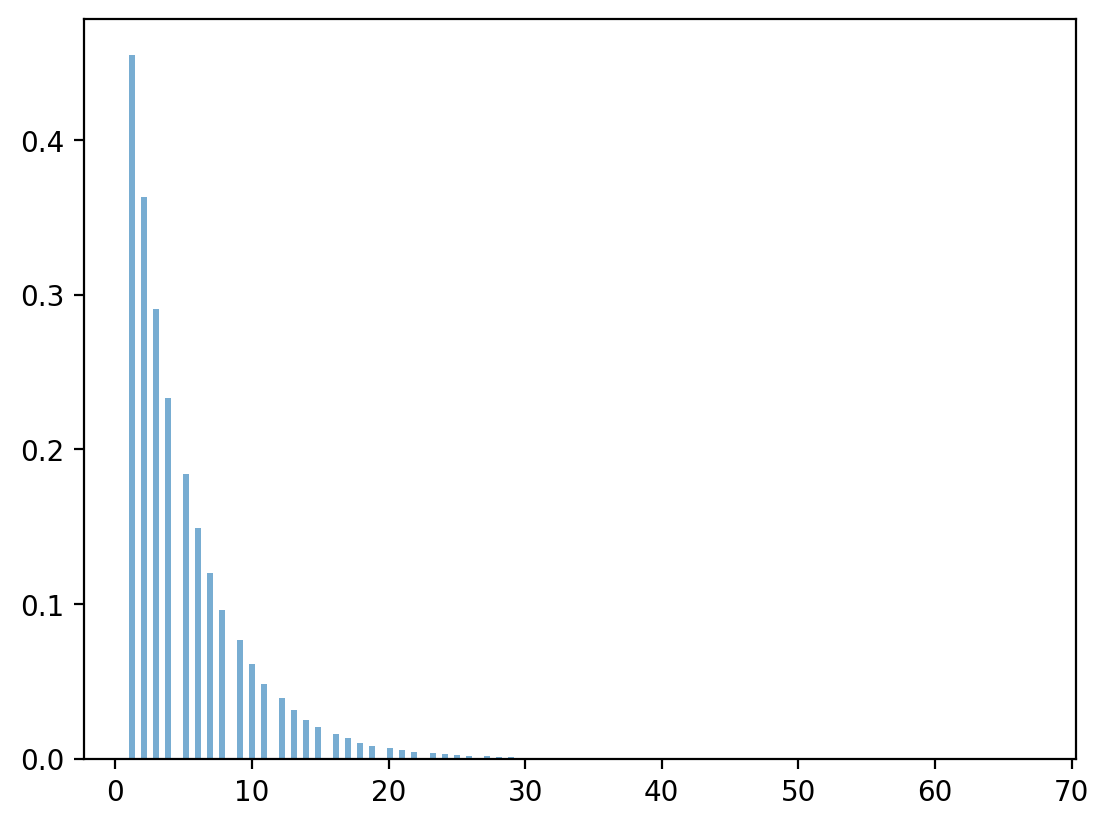

9.2. Geometric distribution#

A discrete geometric distribution has probability mass function

where

The mean and variance of this one-parameter probability distribution are

Let’s use Python draw observations from the distribution and compare the sample mean and variance with the theoretical results.

# specify parameters

p, n = 0.3, 1_000_000

# draw observations from the distribution

x = np.random.geometric(p, n)

# compute sample mean and variance

μ_hat = np.mean(x)

σ2_hat = np.var(x)

print("The sample mean is: ", μ_hat, "\nThe sample variance is: ", σ2_hat)

# compare with theoretical results

print("\nThe population mean is: ", 1/p)

print("The population variance is: ", (1-p)/(p**2))

The sample mean is: 3.334742

The sample variance is: 7.763557793435998

The population mean is: 3.3333333333333335

The population variance is: 7.777777777777778

9.3. Pascal (negative binomial) distribution#

Consider a sequence of independent Bernoulli trials.

Let

Let

Its distribution is

Here, we choose from among

We compute the mean and variance to be

# specify parameters

r, p, n = 10, 0.3, 1_000_000

# draw observations from the distribution

x = np.random.negative_binomial(r, p, n)

# compute sample mean and variance

μ_hat = np.mean(x)

σ2_hat = np.var(x)

print("The sample mean is: ", μ_hat, "\nThe sample variance is: ", σ2_hat)

print("\nThe population mean is: ", r*(1-p)/p)

print("The population variance is: ", r*(1-p)/p**2)

The sample mean is: 23.325444

The sample variance is: 77.83040620286394

The population mean is: 23.333333333333336

The population variance is: 77.77777777777779

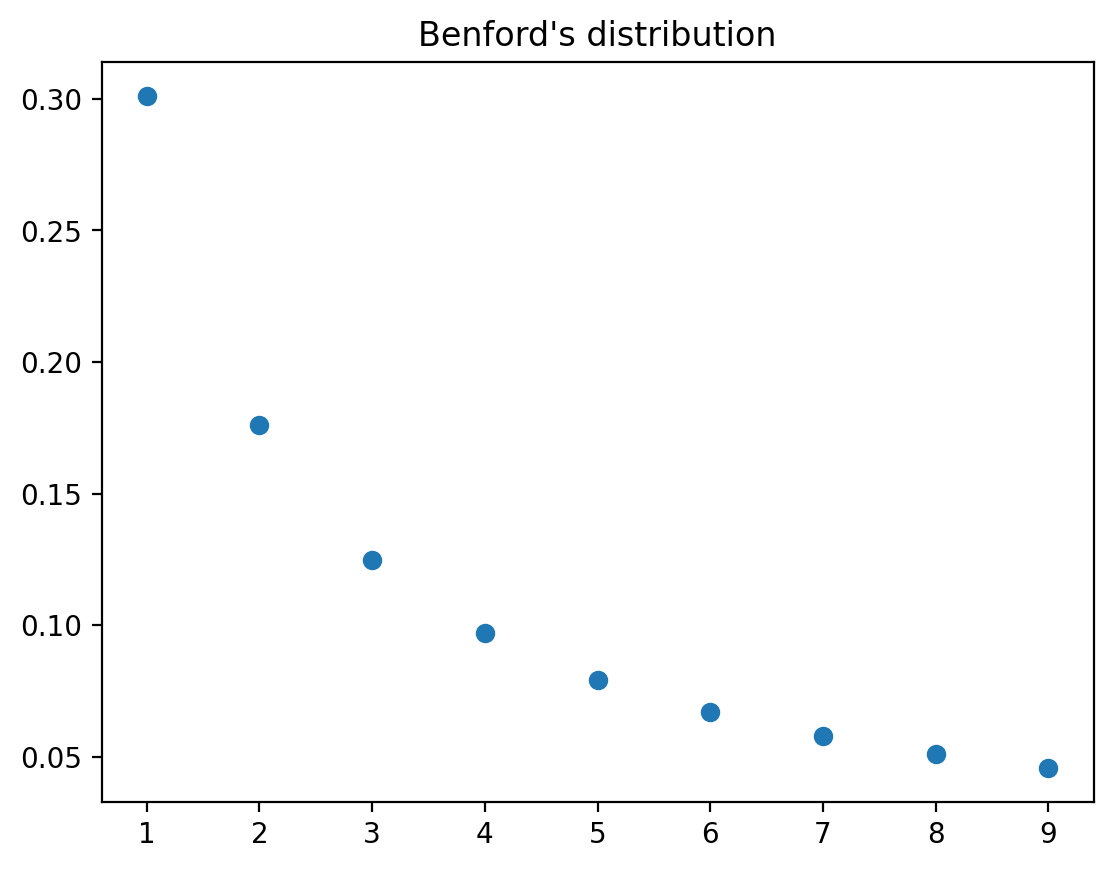

9.4. Newcomb–Benford distribution#

The Newcomb–Benford law fits many data sets, e.g., reports of incomes to tax authorities, in which the leading digit is more likely to be small than large.

See https://en.wikipedia.org/wiki/Benford’s_law

A Benford probability distribution is

where

This is a well defined discrete distribution since we can verify that probabilities are nonnegative and sum to

The mean and variance of a Benford distribution are

We verify the above and compute the mean and variance using numpy.

Benford_pmf = np.array([np.log10(1+1/d) for d in range(1,10)])

k = np.arange(1, 10)

# mean

mean = k @ Benford_pmf

# variance

var = ((k - mean) ** 2) @ Benford_pmf

# verify sum to 1

print(np.sum(Benford_pmf))

print(mean)

print(var)

0.9999999999999999

3.440236967123206

6.056512631375666

# plot distribution

plt.plot(range(1,10), Benford_pmf, 'o')

plt.title('Benford\'s distribution')

plt.show()

Now let’s turn to some continuous random variables.

9.5. Univariate Gaussian distribution#

We write

to indicate the probability distribution

In the below example, we set

# specify parameters

μ, σ = 0, 0.1

# specify number of draws

n = 1_000_000

# draw observations from the distribution

x = np.random.normal(μ, σ, n)

# compute sample mean and variance

μ_hat = np.mean(x)

σ_hat = np.std(x)

print("The sample mean is: ", μ_hat)

print("The sample standard deviation is: ", σ_hat)

The sample mean is: -2.8548065661503377e-05

The sample standard deviation is: 0.09990243468371045

# compare

print(μ-μ_hat < 1e-3)

print(σ-σ_hat < 1e-3)

True

True

9.6. Uniform Distribution#

The population mean and variance are

# specify parameters

a, b = 10, 20

# specify number of draws

n = 1_000_000

# draw observations from the distribution

x = a + (b-a)*np.random.rand(n)

# compute sample mean and variance

μ_hat = np.mean(x)

σ2_hat = np.var(x)

print("The sample mean is: ", μ_hat, "\nThe sample variance is: ", σ2_hat)

print("\nThe population mean is: ", (a+b)/2)

print("The population variance is: ", (b-a)**2/12)

The sample mean is: 15.00250459918252

The sample variance is: 8.342970489200585

The population mean is: 15.0

The population variance is: 8.333333333333334

9.7. A Mixed Discrete-Continuous Distribution#

We’ll motivate this example with a little story.

Suppose that to apply for a job you take an interview and either pass or fail it.

You have

We can describe your daily salary as a discrete-continuous variable with the following probabilities:

Let’s start by generating a random sample and computing sample moments.

x = np.random.rand(1_000_000)

# x[x > 0.95] = 100*x[x > 0.95]+300

x[x > 0.95] = 100*np.random.rand(len(x[x > 0.95]))+300

x[x <= 0.95] = 0

μ_hat = np.mean(x)

σ2_hat = np.var(x)

print("The sample mean is: ", μ_hat, "\nThe sample variance is: ", σ2_hat)

The sample mean is: 17.536613589301137

The sample variance is: 5874.314525073605

The analytical mean and variance can be computed:

mean = 0.0005*0.5*(400**2 - 300**2)

var = 0.95*17.5**2+0.0005/3*((400-17.5)**3-(300-17.5)**3)

print("mean: ", mean)

print("variance: ", var)

mean: 17.5

variance: 5860.416666666666

9.8. Drawing a Random Number from a Particular Distribution#

Suppose we have at our disposal a pseudo random number that draws a uniform random variable, i.e., one with probability distribution

How can we transform

The key tool is the inverse of a cumulative distribution function (CDF).

Observe that the CDF of a distribution is monotone and non-decreasing, taking values between

We can draw a sample of a random variable

draw a random variable

pass the sample value of

Thus, knowing the “inverse” CDF of a distribution is enough to simulate from this distribution.

Note

The “inverse” CDF needs to exist for this method to work.

The inverse CDF is

Here we use infimum because a CDF is a non-decreasing and right-continuous function.

Thus, suppose that

We want to sample a random variable

It turns out that if we use draw uniform random numbers

then

We’ll verify this in the special case in which

Note that

where the last equality occurs because

Let’s use numpy to compute some examples.

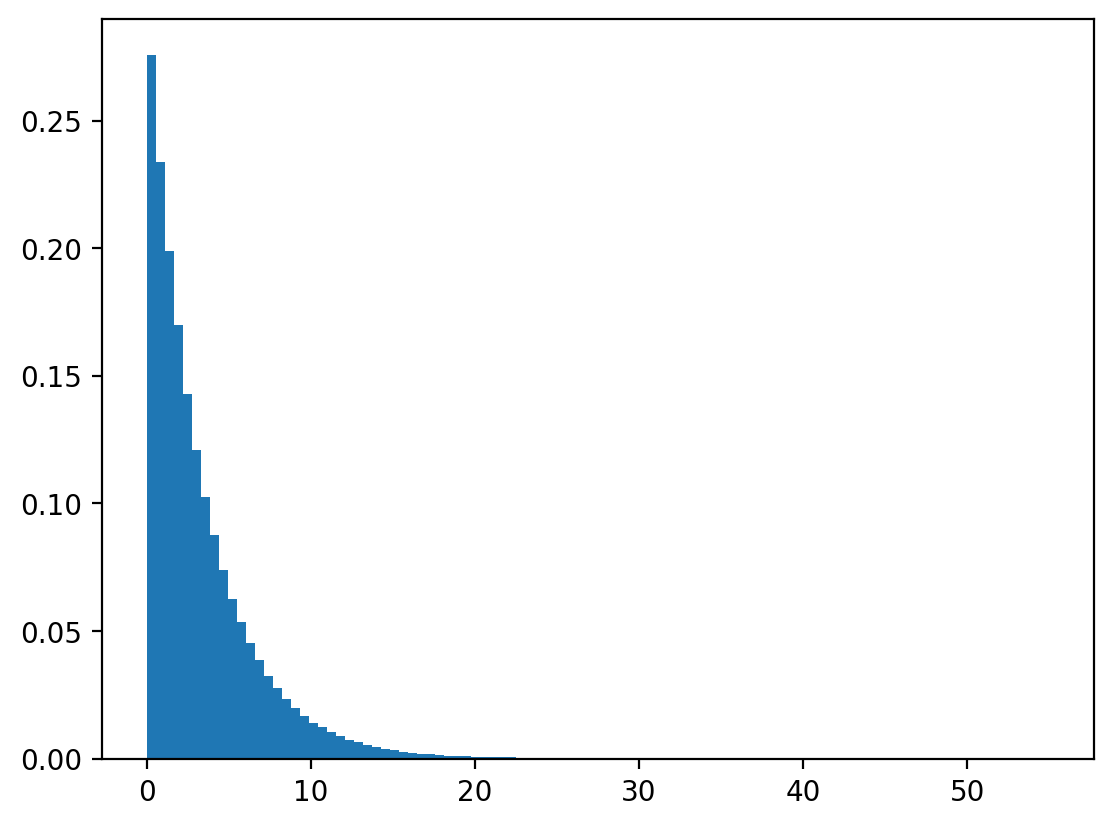

Example: A continuous geometric (exponential) distribution

Let

Its density function is

Its CDF is

Let

The distribution

Let’s draw

We’ll check whether

Let’s check with numpy.

n, λ = 1_000_000, 0.3

# draw uniform numbers

u = np.random.rand(n)

# transform

x = -np.log(1-u)/λ

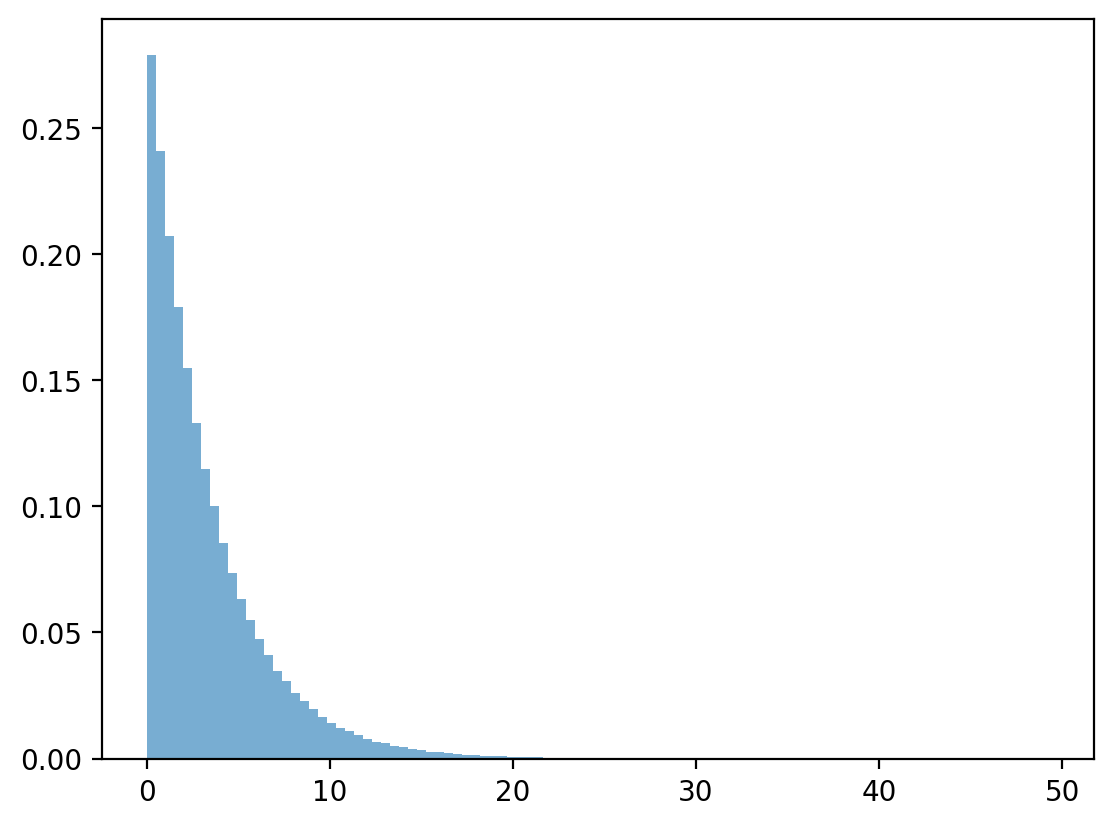

# draw geometric distributions

x_g = np.random.exponential(1 / λ, n)

# plot and compare

plt.hist(x, bins=100, density=True)

plt.show()

plt.hist(x_g, bins=100, density=True, alpha=0.6)

plt.show()

Geometric distribution

Let

Its CDF is given by

Again, let

Let’s deduce the distribution of

However,

So let

where

Thus

We can verify that numpy program.

Note

The exponential distribution is the continuous analog of geometric distribution.

n, λ = 1_000_000, 0.8

# draw uniform numbers

u = np.random.rand(n)

# transform

x = np.ceil(np.log(1-u)/np.log(λ) - 1)

# draw geometric distributions

x_g = np.random.geometric(1-λ, n)

# plot and compare

plt.hist(x, bins=150, density=True)

plt.show()

np.random.geometric(1-λ, n).max()

np.int64(74)

np.log(0.4)/np.log(0.3)

np.float64(0.7610560044063083)

plt.hist(x_g, bins=150, density=True, alpha=0.6)

plt.show()